Capital Adequacy

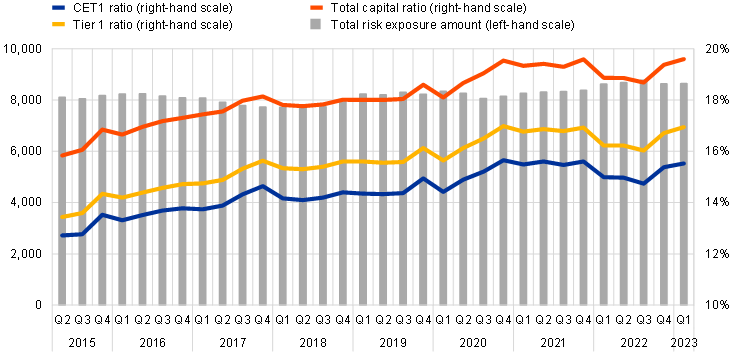

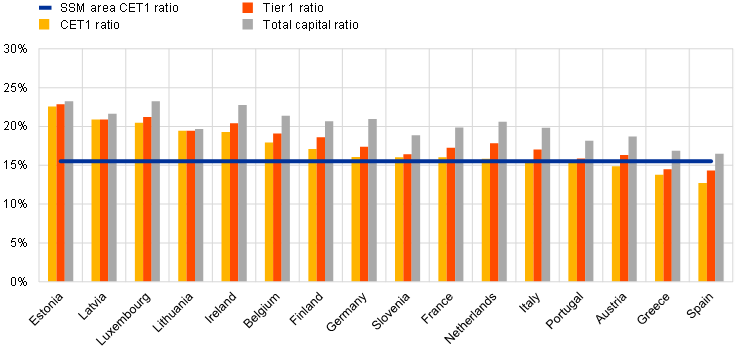

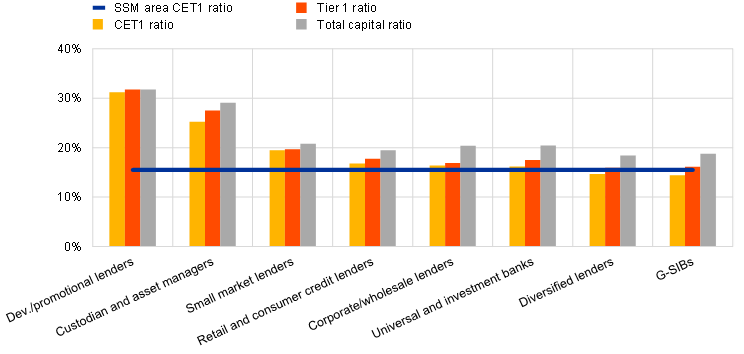

The aggregate capital ratios of significant institutions (i.e. those banks that are supervised directly by the ECB) increased in the first quarter of 2023. The aggregate Common Equity Tier 1 (CET1) ratio stood at 15.53%, the aggregate Tier 1 ratio stood at 16.94% and the aggregate total capital ratio stood at 19.60%. Aggregate CET1 ratios at country level ranged from 12.71% in Spain to 22.56% in Estonia. Across Single Supervisory Mechanism business model categories, global systemically important banks (G-SIBs) reported the lowest aggregate CET1 ratio (14.45%) and development/promotional lenders reported the highest (31.19%).

Chart 1

Capital ratios and their components by reference period

(EUR billions; percentages)

Source: ECB.

Chart 2

Capital ratios by home country for the first quarter of 2023

(percentages)

Source: ECB.

Note: Some countries participating in European banking supervision are not included in this chart, either for confidentiality reasons or because there are no significant institutions at the highest level of consolidation in that country.

Chart 3

Capital ratios by business model for the first quarter of 2023

(percentages)

Source: ECB. Notes: “G-SIBs” stands for global systemically important banks. “Dev./promotional lenders” stands for development/promotional lenders.

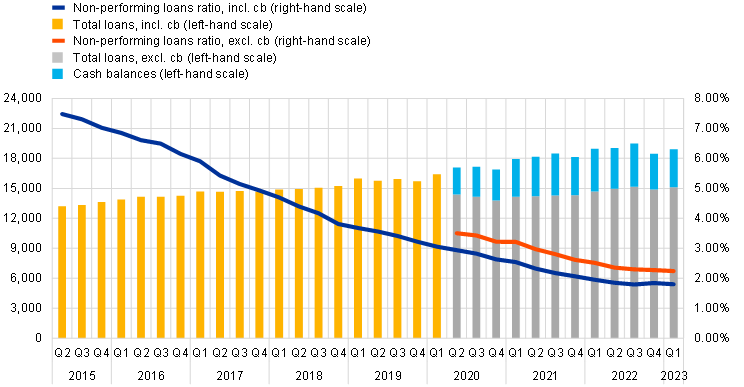

Asset quality

The non-performing loans (NPL) ratio excluding cash balances at central banks and other demand deposits slightly decreased to 2.24% in the first quarter of 2023. The stock of NPLs (numerator) remained stable at €339 billion while loans and advances excluding cash balances (denominator) slightly increased to €15,115 billion.

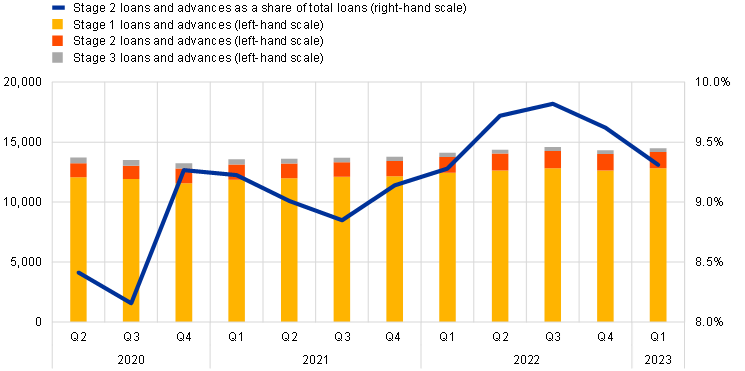

Aggregate stage 2 loans as a share of total loans decreased to 9.31% (down from 9.62% in the previous quarter). The stock of stage 2 loans amounted to €1,351 billion (compared with €1,380 billion in the previous quarter).

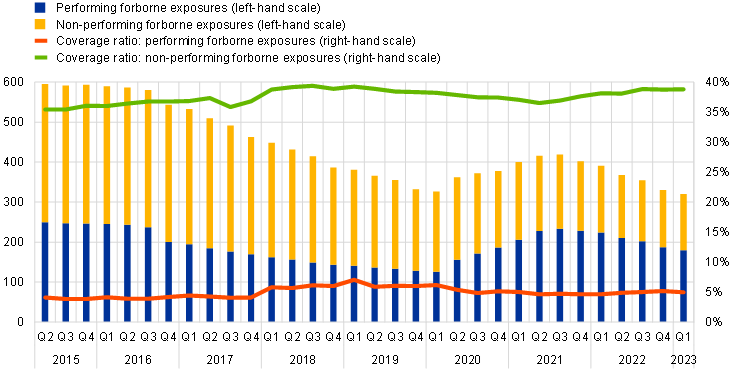

Forborne exposures decreased slightly to €321 billion in the first quarter (compared with €331 billion in the previous quarter and €391 billion one year ago), while their coverage ratios remained largely stable (4.98% for performing forborne exposures and 38.82% for non-performing forborne exposures).

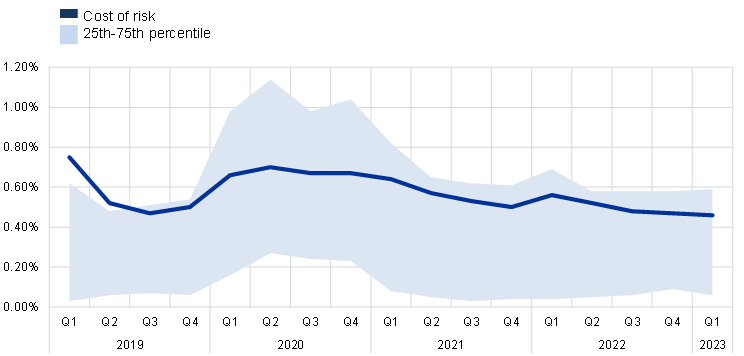

Cost of risk was stable at an aggregate level of 0.46% in the first quarter of 2023 (compared with 0.47% in the previous quarter). Across significant institutions, the interquartile range widened to 0.53 percentage points (up from 0.49 percentage points in the previous quarter).

Chart 4

Non-performing loans by reference period

(EUR billions; percentages)

Source: ECB. Note: “cb” stands for cash balances at central banks and other demand deposits.

Chart 5

Loans and advances subject to impairment review by reference period

(EUR billions; percentages)

Source: ECB.

Note: Stage 1 includes assets where credit risk has not increased significantly since initial recognition, Stage 2 includes assets that have had a significant increase in credit risk since initial recognition, and Stage 3 includes assets that have objective evidence of impairment at the reporting date.

Chart 6

Loans and advances subject to forbearance measures by reference period

(EUR billions; percentages)

Source: ECB.

Chart 7

Cost of risk by reference period

(percentages)

Source: ECB.

Return on Equity

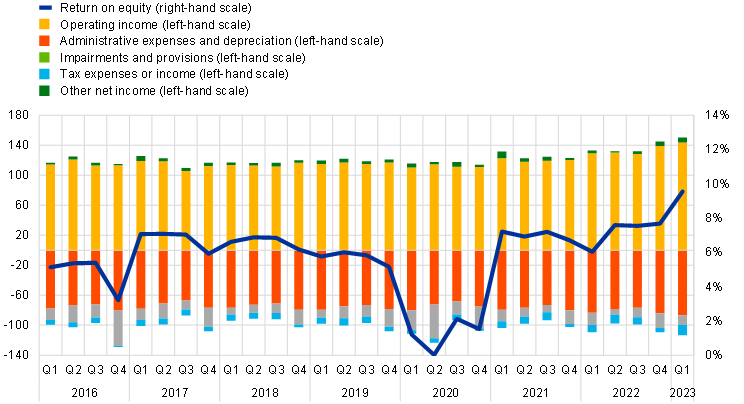

The aggregated annualised return on equity increased significantly to 9.56% in the first quarter of 2023 (compared with 7.68% for the full year in 2022). Increase in operating income (driven by higher net interest income which rose by 24% year-on-year) and decrease in impairment and provisions were the main contributors of aggregate net profit (the numerator of the return on equity). In the first quarter of 2023 the net interest margin increased to 1.48% (compared with 1.36% in the previous quarter and 1.20% one year ago), while still showing important structural differences across countries.

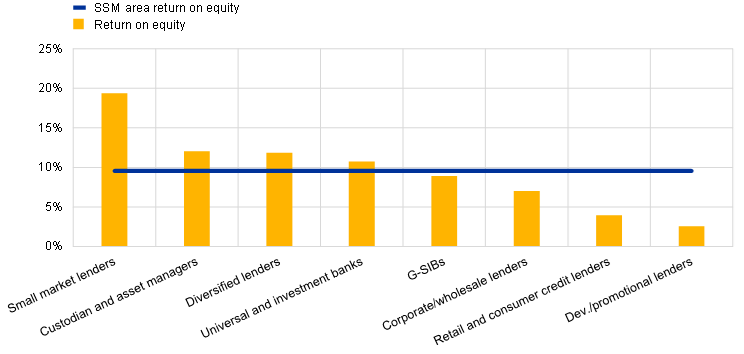

Across Single Supervisory Mechanism business model categories, the aggregate annualised return on equity ranged from 2.56% for development/promotional lenders to 19.37% for small market lenders.

Chart 8

Return on equity and composition of net profit and loss by reference period

(EUR billions; percentages)

Source: ECB.

Chart 9

Return on equity by business model for the first quarter of 2023

(percentages)

Source: ECB. Note: “G-SIBs” stands for global systemically important banks. “Dev./promotional lenders” stands for Development/promotional lenders.

Liquidity and Funding

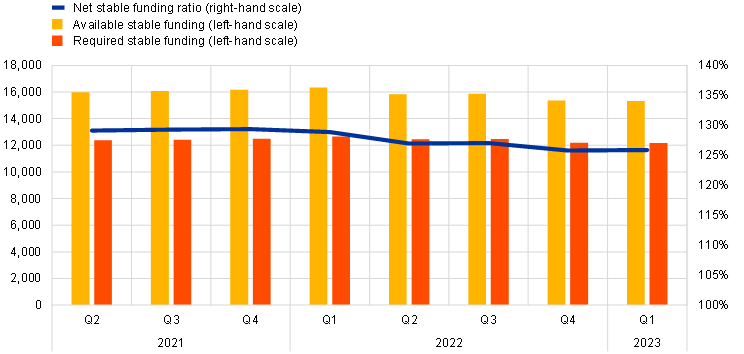

The liquidity coverage ratio stood stable at 161.27% in the first quarter of 2023 (compared with 161.32% in the previous quarter and 167.39% in the first quarter of 2022). The net stable funding ratio remained stable at 125.87% (compared with 125.79% in the previous quarter and 128.88% in the first quarter of 2022).

Chart 10

Liquidity coverage ratio and its components by reference period

(EUR billions; percentages)

Source: ECB.

Chart 11

Net stable funding ratio and its components by reference period

(EUR billions; percentages)

Source: ECB.

Factors Affecting Changes

Supervisory banking statistics are calculated by aggregating the data that are reported by banks which report COREP (capital adequacy information) and FINREP (financial information) at the relevant point in time. Consequently, changes from one quarter to the next can be influenced by the following factors:

- changes in the sample of reporting institutions;

- mergers and acquisitions;

- reclassifications (e.g. portfolio shifts as a result of certain assets being reclassified from one accounting portfolio to another).