As a regulator, the MFSA is dedicated to safeguarding the interests of consumers of financial services as well as ensuring market integrity. One of the ways in which we accomplish this mission is through educational campaigns aimed at helping consumers to achieve their financial goals and protecting them as the investment world becomes increasingly dynamic.

Investor Education empowers the general public with the tools, skill and knowledge to make sound financial decisions throughout life, making investment products more accessible and inclusive.

In line with this, we have embarked on a programme with the objective to raise awareness and provide an educational platform pertaining to financial investment.

This page includes frequently asked questions (FAQs) and answers related to financial investments, including those with a focus on Sustainable Finance.

What should I do before making any investment decision?

Before making investment decisions you must empower yourself through information about the risks and rewards of investing. This can help you avoid any potential losses.

As a smart investor:

- Ask questions. Do not make rapid investment decisions without considering your long-term financial goals.

- Avoid circumstances that can lead to fraud. Make sure the firm you are dealing with is authorised to provide investment services in Malta by the MFSA and/or by an EU Financial Services Authority. Please check by searching the Company on the Financial Services Register at the following link: https://www.mfsa.mt/financial-services-register/.

- Consider alternatives. Prior to committing to a particular Investment Services Provider, do consider what other authorised Investment Services Providers are offering in terms of service and value.

- Bear in mind that past performance is no guarantee of future returns.

- Be mindful of the investment service that you are being offered. Ask the representative of the authorised Investment Services Provider to explain to you the difference between an advisory and a non-advisory investment service.

- Read all documents carefully and obtain clarifications in case of need especially before signing-off any documentation. Always keep copies of all investment documentation.

- Be informed about all costs and associated charges in relation to the provision of investment services, including the cost of the financial instrument recommended or marketed to you. In relation to investment advisory services, you should also be provided with the cost of the advice.

- Remember that you may have to pay taxes on any profits you make.

- Get adequate reports on the investment services provided and ensure that you read through them.

- Take note of the authorised Investment Services Provider’s Complaints Policy.

What type of investment services are available and what should I expect?

You should be aware that different investment services are available, according to the degree of support (if any) you are looking for.

Typically, the most common forms of investment services are the following:

- The provision of investment advice whereby investors are provided with personal recommendations on the investments products that would be suitable for them (i.e. advisory service and portfolio management);

- The purchase or sale of financial products on a non-advisory basis (therefore without receiving investment advice); or

- The purchase or sale of financial products on an execution-only basis

If you opt for investment advisory services and portfolio management services, the investment firm’s representative will ask you several questions to understand your investment objectives (including your attitude to risk), your knowledge and experience and your financial circumstances so that he/she can select a suitable financial instrument or investment portfolio. These questions form part of the Suitability Test. It is in your best interest to provide all relevant information to the authorised firm’s representative. In the case of investment advisory service, do make sure that you are provided with a copy of the Suitability Report, before proceeding with the transaction. This document should outline how the advice meets your investment preferences, objectives and other characteristics.

If you want an investment firm to buy or sell on your behalf a financial product without providing you with advisory or portfolio management services, you will only be asked questions on your knowledge and experience relating to the specific investment. This is referred to as the Appropriateness Test. You may be provided with warnings in case the product is not appropriate for you or the information provided is not sufficient to determine the appropriateness or otherwise of the financial product.

In certain instances, and only for some types of financial instruments (referred to as “non-complex products”), you may invest without even being subject to the Appropriateness Test. This service is referred to as Execution Only service. In this case the firm will warn you that is not exercising any judgement on your behalf.

What does the term ‘nominee’ mean?

A nominee service means that an investment firm is authorised to hold your funds and investments on your behalf in separately designated clients’ money and clients’ asset accounts. These accounts are ringfenced from the Company’s own accounts. Nominees will act according to your instructions. It is important to ask the representatives of the investment firm if your funds and assets will be held in a nominee account before you start investing.

Do I have to pay fees for investing in a financial product?

Depending on the product and/or service you may be required to pay different costs and charges that will be disclosed to you before you take an investment decision. It is important that you understand the costs and are aware of the impact that the fees you have paid, or that you will be required to pay, have on the investments, especially on the return that you expect from it. Fees should be communicated in a timely manner, be complete and easy to understand and should make it easy for you to compare such charges with alternative products available in the marketplace.

Can I invest without risk?

The short answer is “no”. When investing, you will always be exposed to a certain amount of risk. It is important that you remember that, in general, higher and more tempting returns mean higher risks. Before you invest, you must carefully consider the risk which you may be exposed to.

There are, however, ways to reduce risk.

- Be wary of investment schemes that are presented in a way to make you believe that there are no risks related to the investment (such as “get rich quick”, “can’t lose”, etc..)

- Do your own research, even if the product you want to invest in has been endorsed by a celebrity or an influencer.

- Know your timing. If you will need your money in the near future, it might not be a good idea to invest in the stock market as if there are any drops in value, there may not be enough time to regain the original value.

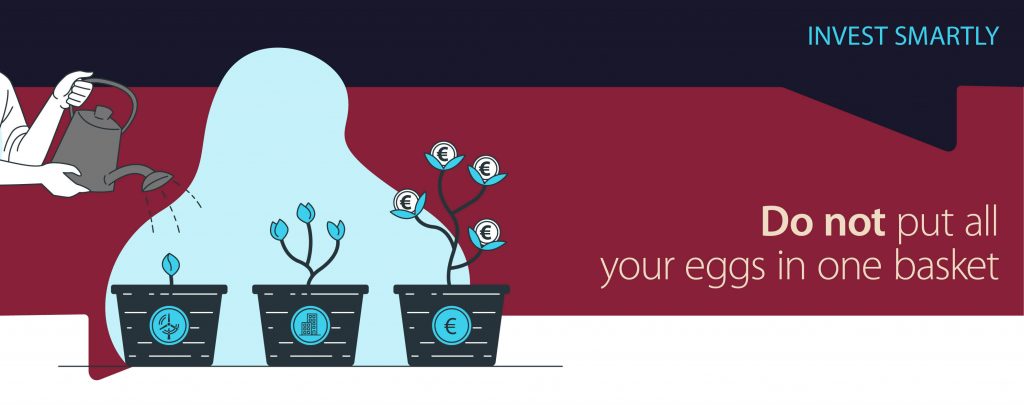

- Diversify your investment. Put your eggs into different baskets so that if one gets dropped, you don’t lose everything. Regularly check your portfolio.

- If you need help, speak to a professional financial adviser.

What does portfolio diversification mean?

A smart investor does not put all his eggs in one basket. The main benefit of portfolio diversification is to lower the risk of a single event from harming your investments. A diverse portfolio may include a combination of investments such as stocks and bonds issued by different companies operating in different industries, currencies and commodities.

Even if you observe that your investments are performing well, you should be aware that past performance is not indicative of future results, and that is why you should protect yourself from adverse market cycles and volatility through portfolio diversification. An optimally diverse investment portfolio will help you generate good returns and preserve your wealth.

I would like to invest in crypto-assets, is there anything I should be aware of?

With crypto assets all over the news it’s tempting to dive right in. Crypto-assets are digital assets being a digital representations of value that can be transferred, stored and traded electronically by using cryptographic techniques.

These are risky investments whose value can change rapidly and unpredictably. Examples of crypto-assets are the Initial Coin Offerings (ICOs), which are often issued by startups as a fundraising method. When dealing with crypto-assets, given the decentralised and anonymous nature of these instruments, you should look for as much information as possible, with particular reference to the identity of the issuer and refrain from investing if you do not have sufficient knowledge to understand the nature of these products and/or detect any red flag that could possibly lead to scam or fraud.

Local bonds and shares listed on the Malta Stock Exchange are approved by the MFSA, does this mean that they are risk free and that my capital is guaranteed?

No. The MFSA checks that the information included in the prospectus meets the standards of completeness, comprehensibility and consistency required by European law and that the company issuing those bonds satisfy the conditions stated in the Capital Markets Rules. All investments carry risk. In general, higher returns mean higher risks.

Remember that an investment in local bonds and shares are NOT covered by any guaranteed schemes.

What is the difference between a guarantee and a security?

These two distinct terms are sometimes used interchangeably. In simple terms, a guarantee is a “promise” by another person usually an operating company within the same group as the issuer, to honour the payment of Bond interest and principal, should the issuer fail to pay the bondholders.

On the other hand, a security takes the form of an issuer’s assets which is segregated from the rest of its assets and held by a third party, usually a security trustee, to be sold or used to the benefit of the bondholders, should the issuer fail to pay bond interest and/or the principal.

Always look out for dependencies between the guarantor and the issuer as sometimes the failure of an issuer to pay its dues means that the guarantor is not in a very good financial position.

Can I lose my capital even if the bonds are guaranteed or secured?

Yes. If there is a good chance that the security loses its value or that the guarantor’s business fails, then there is a risk that you lose part or the full amount being invested. It is important that you understand the value of the security and the guarantee when investing in the first place.

Look for the risk factors relating to the guarantee and security which are indicated in bold in the prospectus.

Where can I find relevant information when investing in local bonds listed on the Malta Stock Exchange?

Companies issuing bonds to be listed on the Malta Stock Exchange need to prepare a prospectus. This document may be lengthy but provides a lot of information which would help you make your investment decision.

Always base your decisions on formal information such as prospectus and company announcements issued by the company rather than hearsay, newspaper articles and information on social media platforms.

What should I do if I get to know that the company I invested in is in financial trouble?

Do not panic and do not take hasty investment decisions like selling off your investment. It is important to gather all the information available to you through formal channels of communication such as company announcements, circulars sent by the company and financial statements issued by the company. Once you have all the information, assess your position and take your decision. If you are not sure about the decision, consider speaking to an investment adviser to assist you.

Always keep up to date with the affairs of the company in which you have invested. Listed companies on the Malta Stock Exchange must have a section dedicated to Investors Relations on their website.